亲爱的FRM学员:欢迎来到融跃教育FRM网!

距离2026年5月9日FRM一级考期还有 天!

全国热线:400-963-0708

全国热线:400-963-0708  网站地图

网站地图

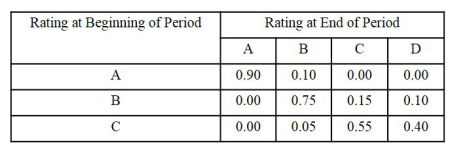

As a result of the credit crunch, a small retail bank wants to better predict and model the likelihood that its larger commercial loans might default. It is developing an internal ratings-based approach to assess its commercial customers. Given this one-year transition matrix, what is the probability that a loan currently rated at B will default over a two-year period?

A17.50%

B20.0%

C21.1%

D23.5%

打开微信扫一扫

添加FRM讲师

课程咨询热线

400-963-0708

微信扫一扫

还没有找到合适的FRM课程?赶快联系学管老师,让老师马上联系您! 试听FRM培训课程 ,高通过省时省心!

行业动态

行业动态 职业发展

职业发展 融跃动态

融跃动态 FRM协会动态

FRM协会动态 FRM最新公告

FRM最新公告